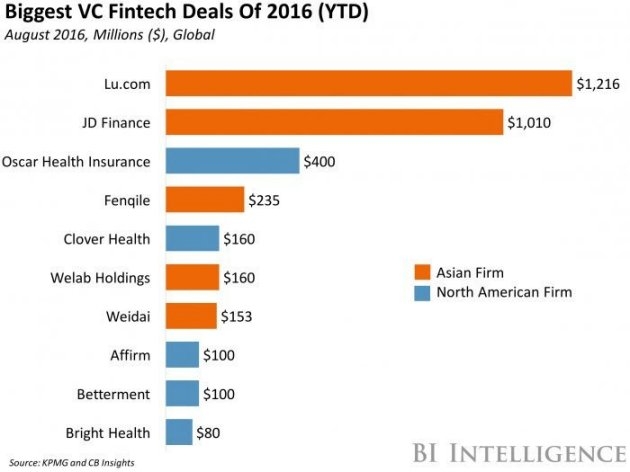

According to reports from Leifeng.com, KPMG and CB Insights, the data provider of the venture capital industry, released a major financing report for the Fintech industry in the second quarter of this year. The report points out that globally, there were approximately 2.5 billion U.S. dollar investment in the first half of the year. The company flocked to Fintech Ventures, and the total amount of funds entering the Fintech field reached US$9.4 billion. The B round of financing of domestic ant gold suits of up to US$4.5 billion has greatly boosted the financing level of Fintech.

It is noteworthy that according to the report list, five of the top ten Fintech venture financing transactions are from China, one of which is from Hong Kong, and the largest two ventures are ventures—two Chinese companies: Lukin. And Jingdong Finance - the total amount of transactions add up to even more than the remaining eight total transactions. Ant Financial's $4.5 billion financing is not included in this list because it is not supported by venture capital. If it counts, Gwangju has rolled out the top ten transactions in total. While China's Fintech sector is in full swing, the North American region has experienced a sharp decline. Among them, three of the companies on the list still come from the more emerging areas of insurance technology.

A large amount of capital flocked to China's Fintech company and was consistent with the previous survey of global Fintech unicorns — the most valuable of Fintech's four-fifths came from China. However, domestic Fintech startups started much later than abroad, such as the United States financial technology star Lending Club, the company was founded at least 10 years, IPO in 2014. On the other hand, in China, even earlier Internet finance, the real rise of the country has not yet reached four or five years. Fintech's concept—it means that technology has changed its financial services. It has only recently been introduced to the domestic market in the last year or two. Why did China Fintech start so late but did it develop so rapidly? In this regard , Lei Feng Network (search "Lei Feng Net" public concern) consulted some people in the industry, including academic experts, investors and entrepreneurs in the industry.

First of all, what is FintechFintech is an exotic word, which can be understood as “finance+technologyâ€. Originally, it means “finance and technologyâ€. Its core is the use of technology to drive innovation in financial services. According to Wikipedia: Fintech is a business model that uses high technology to make financial services more efficient.

Nowadays, we are familiar with Internet finance, although many companies in this field begin to talk about financial technology, but they are not FinTech company, and part of the development of big data, artificial intelligence to do credit and risk control can be described as Fintech innovation. Therefore, the industry also calls for users to be alert to P2P scams.

So far, Fintech is divided into several sub-fields. The technologies that are currently playing a role in improving the effectiveness of the financial sector include big data, cloud computing, artificial intelligence, and blockchain. They are used in credit information, risk management and control, smart investment and wealth management, and new types of payments, such as big data analysis. Artificial intelligence credit and risk control, robot investment consultants; decentralized payment based on blockchain technology, digital currency settlement in the financial industry, etc. Do not repeat them here.

Therefore, why can such a new type of technology application achieve rapid development in the country in the short term?

market"The era of domestic low-risk arbitrage is over."

In the list of KPMG and CB Insights, five Chinese companies were listed on the list, two of which, Lu Jinsuo and Jingdong Finance, were the main players, at least for the time being in the smart investment advisory business. Regarding the phenomena that Fintech’s most dazzling sub-sector, Robo-Advisor, broke out in the country in the past year, Ye Xin, the financial whale CEO of domestic smart investment startups , said that with the end of the domestic economy, high growth has entered the structural adjustment. During the period, the over-expansion of debt, and the reform of exchange rates and capital projects, the domestic high-net-worth population gradually generated the demand for overseas asset allocation. In fact, according to statistics, since the QDII total amount has remained unchanged at $89.99 billion since March of last year, QDII quotas have become extremely tight as investors’ enthusiasm for overseas investment has increased.

“The era of low-risk arbitrage in China has passed, and the professional capabilities required for investment and wealth management of general investors have also put forward higher requirements.†However, “Chinese investors’ experience in overseas asset allocation is relatively lacking, and they are not suitable for overseas markets and investment targets. Also relatively unfamiliar."

Therefore, ordinary investors need more professional guidance. Traditional investment and financing agencies cannot take care of these customers. Therefore, smart investment advice (robot financing) is needed to solve the problems of efficiency and general welfare.

Ye Xin pointed out that there were many reasons why the former had failed to develop intelligent investment advice. Most importantly, the past market is full of low-risk arbitrage opportunities, such as real estate in the past two decades, bonds in the past 10 years, trusts in the past eight years, financial management in the past seven years, P2P in the past three years, etc. In an uncomplicated, easy-to-earn market environment, there is no need for investment consultants. On the contrary, what the market needs more is how to get the opportunity faster and more effectively. It is the seller's broker. However, when the era of simple arbitrage is over, users are forced to face a complex market that needs to face the severe test of “what can we buy without losing money†or even “buy nothing?†This requires professional competence. The investment advisor came to respond, and investment advisors have value.

Similarly, Ma Yongfu, a financial advisor for intelligent advisors, said:

In the past few years, what happened to China's wealth managers all over the world is low-risk and high-yield, but this phenomenon is changing and the fixed-income market is undergoing a decline. The so-called decline refers to the decline in the yield, collapse refers to a series of default risk events, and this trend will accelerate. This will lead to financial management shifting from fixed income to floating profit. This means that various financial strategies and financial tools will be popular in the future.

User needsHuge market demand and growth momentum

As for the reasons for the rapid development of China's Fintech, the new president and CEO and associate professor Chang Hong said that this is related to China's entrepreneurial innovation atmosphere and environment, and related to China's huge market demand and growth momentum.

According to Lei Fengnet’s previous report, McKinsey’s data points out that 59% of the Asian population and 876 million people are unbanked. However, it is interesting that Asian Internet users account for nearly half of the world. Coupled with the number of Asian digital banking consumers will reach 1.7 billion by 2020 - this brings a lot of opportunities for Fintech start-ups, and there are a lot of problems worth solving.

These issues include small microfinance, new payment instruments, big data credits, and risk control. Of the five venture capital winners on the list, almost all involved micro-loans.

According to Accenture's latest data, investment in the Fintech field in the Asia-Pacific region has increased from 800 million U.S. dollars in 2014 to 3.5 billion U.S. dollars in 2015. More and more VCs have turned their attention to Asian financial technology startups, and financial institutions have shown increasing interest in this area.

Undoubtedly, China is one of the main market forces.

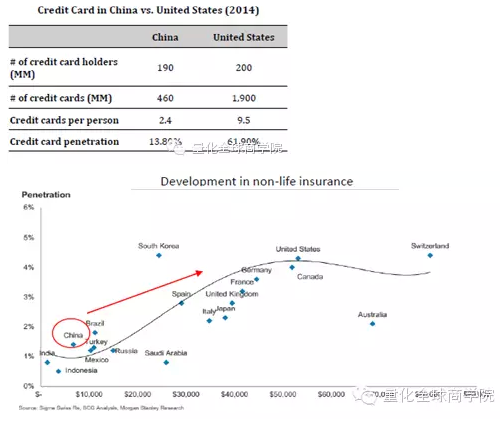

There are sound pension systems in foreign countries. Relative laws and regulations in Europe and the United States are relatively complete and suitable for long-term investment. Investors are also more able to accept short-term investment fluctuations. In contrast, an analysis by Xie Yan from the University of North Carolina MBA and the Bachelor of Finance at the University of International Business and Economics said that data from the national credit card penetration rate and insurance penetration rate indicate that Chinese consumers have the highest degree of acceptance of online investment and promotion. of.

systemThe institutional demand can not meet the huge demand

Wen Xiangyun, director of financial marketing at Qianxiang, pointed out that in China, financial technology has more market space. "Because China's financial system is not very sound, it gives financial science and technology growth space. China's traditional financial institutions have not been able to cover a large number of small and medium-sized users, mainly serving state-owned listed companies and large-scale private enterprises." At the same time, "Because, The U.S. financial system is relatively developed, and all kinds of customers basically have financial institutions in place. "

WJ Capital Ping Muchuan analyzed:

Traditional Chinese financial service institutions have too many users for whom they are unwilling or unable to receive them. However, the demand for these users is very strong. Chinese financial technology companies use technology to serve these users and meet their financial needs. China's Fintech business is developing rapidly.

Supervision

Thunder Hao, the founder of the Thunder, recently commented on the newly issued new rules for online loans. Cheng Hao announced the resignation on the thirteenth anniversary of the founding of Thunder, and Li Wei and Wang Yang of Song Sheng Capital established a fund called Song Yuan Yuan Wang, and the main angel to the A round. He pointed out that the biggest difference between the regulatory culture of China and the United States is that:

In the United States, if there are no laws and regulations, you have done so. The state has enacted new laws and regulations to cover leaks, and then it has never been done. Afterwards, everybody should do it according to the new laws and regulations;

In China, if you do not have laws and regulations, and you do things that essentially cause harm, then it is still easy to govern under existing regulations. After all, domestic laws and regulations are extensive and vague.

If your essence is good-natured and there are no harm consequences, domestic supervision is still very friendly, and it is more beneficial to domestic Fintech startups. This is also the reason why China's Fintech has grown even faster than the United States.

In the wave of Fintech, financial technology and smart investment are still at the starting stage. Whether it is financial technology or internet finance, the essence lies in finance. In this data-driven financial industry, although the American market has been nurtured for hundreds of years, the overall data conditions are superior to those of China, providing a very good data base for Internet finance startup companies. However, Xie Yan pointed out in the “Rational Differences and Opportunities in Internet Finance between China and the United Statesâ€.

With the acceleration of technological and consumer habits, both in size and environment, the value of data accumulated in the last Internet-based financial era seems to be lower than people's expectations. Those models that are considered to be advanced are far from being able to find the value of data. So far, so-called intelligence seems so clumsy today. However, Chinese enterprises without these legacy restrictions can adapt to the needs of the Internet era more quickly, and innovate more flexibly and boldly in the process of rapid trial and error iterations.

Frequency Inverters, also known as Variable Frequency Inverters or Variable Speed Drives, are electronic devices that are used to control the speed of an electric motor. They convert the incoming AC power into DC power and then back to AC power at the desired frequency and voltage. These devices are commonly used in industrial and commercial applications to regulate the speed of machines and equipment. Low Power Inverters, on the other hand, are designed for use in smaller applications such as home appliances and small machinery. They are typically less expensive and have a lower power output compared to their industrial counterparts. Overall, Frequency Inverters and Variable Frequency Inverters are essential components in modern industrial and commercial applications, while Low Power Inverters are more commonly used in smaller scale applications.

Frequency Inverter,Variable Frequency Inverter,Low Power Inverter,Variable Speed Drive

Frequency Inverter,Variable Frequency Inverter,Low Power Inverter,Variable Speed Drive

WuXi Spread Electrical Co.,LTD , https://www.vfdspread.com